KSeF 2026: old-style invoicing without penalties, but with 2027 risk

Learn when an invoice outside KSeF is an exemption, when it is an offline mode and when it becomes a compliance risk.

Article Summary

In 2026, the absence of KSeF financial penalties does not mean that KSeF is optional. If a taxpayer is already covered by mandatory structured invoicing, a standard B2B invoice should be issued through KSeF unless an exemption or special mode applies.

An invoice received outside KSeF does not automatically remove the buyer's right to deduct VAT. The Polish Ministry of Finance points to the general VAT deduction conditions and the absence of negative premises, but the document should still be treated as a risk signal.

From 1 January 2027, KSeF penalties are expected to apply. 2026 should therefore be used as an implementation period, not as a reason to postpone the process.

Three Different Situations

The phrase old-style invoicing is convenient, but in KSeF it can be misleading. It may describe three very different scenarios: a legal exemption, a legal special mode, or a breach of the mandatory KSeF rules.

The first scenario is an exemption. Examples include B2C invoices, selected statutory exclusions and temporary 2026 rules, such as the PLN 10,000 gross monthly threshold for the smallest taxpayers.

The second scenario is offline24, outage or unavailability of KSeF. The invoice may then be created outside the system, but this is not a return to any PDF chosen by the seller. The document must follow the rules and be submitted to KSeF within the statutory deadline.

The third scenario is a regular breach: a seller covered by mandatory KSeF sends a PDF or paper invoice even though the document should be a structured invoice in KSeF and no exemption applies.

| Scenario | Is it an error? | What to do |

|---|---|---|

| KSeF exemption | No, if it fits the rules | Keep the legal basis and transaction evidence. |

| Offline, outage or unavailability mode | No, if the procedure was followed | Prepare correct FA(3) XML, mark the mode and submit the invoice on time. |

| Regular PDF outside KSeF despite the obligation | Yes, this is a risk signal | Clarify the case, check evidence and fix the KSeF process before 2027. |

Who Can Stay Outside KSeF in 2026

Mandatory KSeF is introduced in stages. From 1 February 2026 it applies to taxpayers whose gross sales in 2024 exceeded PLN 200 million. From 1 April 2026 it applies to other taxpayers, with important temporary exceptions.

Until the end of 2026, taxpayers whose monthly gross sales documented by invoices covered by mandatory KSeF do not exceed PLN 10,000 may still issue invoices outside KSeF. This is not a general exemption from preparing for the system, but a temporary deferral for the smallest volumes.

Until the end of 2026, transitional rules also apply to invoices issued using cash registers and to fiscal receipts with the buyer's NIP treated as simplified invoices up to PLN 450 or EUR 100. B2C invoices and other statutory exclusions remain outside mandatory KSeF separately.

| Case | 2026 status | What to check |

|---|---|---|

| Large taxpayer above PLN 200m gross sales in 2024 | Mandatory KSeF from 1 February 2026 | Whether B2B invoices are sent to KSeF. |

| Other taxpayers | Mandatory KSeF from 1 April 2026 | Whether the document is not covered by an exemption. |

| Monthly sales up to PLN 10,000 gross | Deferral until the end of 2026 | Whether the threshold concerns invoices covered by mandatory KSeF. |

| B2C invoices | Outside mandatory KSeF | Whether the buyer is actually a consumer. |

| Special modes | Outside the system only temporarily | Whether the invoice will be submitted on time. |

Does the Buyer Lose VAT Deduction

The practical answer is: do not automatically reject VAT deduction only because the invoice arrived outside KSeF. The official Ministry of Finance FAQ indicates that the buyer may generally deduct VAT if the substantive deduction conditions under Article 86 of the Polish VAT Act are met and no negative premises apply.

This is not a green light to ignore the issue. An invoice outside KSeF from a seller who should use the system is a warning signal. Accounting should check whether the transaction is real, whether the document matches the order, delivery and payment, and whether there are other tax risks.

The buyer does not have to become the controller of the seller's entire KSeF implementation. The buyer should, however, be able to show due diligence, especially for larger amounts, new suppliers or unusual transaction terms.

| Evidence | Why it helps the buyer |

|---|---|

| Order or contract | Shows the business context of the transaction. |

| Delivery or service confirmation | Connects the invoice with a real economic event. |

| Payment confirmation | Helps evidence the economic flow of the transaction. |

| Correspondence with the seller | Shows an attempt to clarify the invoice outside KSeF when needed. |

| Supplier verification | Supports due diligence in higher-risk transactions. |

Issuer Risk in 2026 and from 2027

For 2026, the key point is to separate two things: the KSeF obligation may already exist, while monetary penalties for KSeF-related breaches are expected to apply only from 1 January 2027. This distinction creates many misunderstandings.

An invoice issued outside KSeF despite the obligation does not make the sale disappear from VAT. The issuer should still settle the output tax. The lack of a monetary penalty in 2026 does not remove the tax obligation or the risk of a dispute about the correctness of the process.

From 1 January 2027, the head of the tax office is expected to be able to impose penalties indicated in Article 106ni of the Polish VAT Act. According to the Ministry FAQ, the penalty may reach up to 100% of the VAT amount shown on the invoice, or up to 18.7% of the total amount due for invoices without VAT.

The most important breaches are: not issuing a structured invoice using KSeF despite the obligation, issuing an invoice inconsistent with the required structure during outage or unavailability, and failing to submit an invoice issued in offline24, outage or unavailability mode on time.

| Area | 2026 | From 1 January 2027 |

|---|---|---|

| KSeF obligation | Applies according to the schedule and exemptions | Continues after some transitional reliefs expire. |

| Monetary penalties | According to MF, not applied in the initial period | Expected to apply for statutory breaches. |

| Buyer's VAT deduction | Not automatically lost | Not automatically lost, but due-diligence risk increases. |

| Process importance | Implementation period | KSeF process becomes a risk-control element. |

Questions for Accounting After Receiving an Invoice Outside KSeF

When a company receives an invoice outside KSeF, it is better to avoid both panic and automatic booking. A short question sequence helps separate an exemption from a problem.

1. Was the seller already covered by mandatory KSeF on the invoice issue date?

2. Does the document relate to a B2C transaction or another clear exclusion?

3. Could the seller use the temporary PLN 10,000 gross monthly threshold until the end of 2026?

4. Was the invoice issued in offline24, outage or unavailability mode, and does the seller intend to submit it to KSeF?

5. Do you have transaction evidence: order, delivery, service performance, payment and correspondence?

6. Do the amount, supplier or transaction circumstances require additional verification?

If the answers do not point to an exemption or special mode, mark the case for clarification. In larger organisations, it is worth having a separate status: invoice outside KSeF for review.

Issuer Checklist

Issuers should not wait until penalties start to apply. The cheapest moment to organise the process is 2026, while teams can still test, improve procedures and train without monetary-sanction pressure.

1. Determine which invoices are B2B, which are B2C and which are excluded.

2. Check whether the sales system generates FA(3) XML, not only PDF.

3. Add XML validation before submission to KSeF.

4. Describe the offline24, outage and KSeF unavailability procedure.

5. Decide who is responsible for submitting the invoice to KSeF within the statutory deadline.

6. Archive the KSeF number, UPO and submission status next to the invoice.

7. Train invoice issuers not to treat PDF as the default B2B document.

Buyer Checklist

Buyers should have a simple procedure for invoices received outside KSeF. The goal is not to block every invoice, but to recognise risk sensibly.

1. Check whether the seller could issue the document outside KSeF.

2. Keep transaction and payment evidence.

3. Mark the invoice for clarification if the seller should operate in KSeF.

4. Ask whether the invoice will be submitted to KSeF in offline or outage mode.

5. For large amounts or new suppliers, perform additional supplier verification.

6. Do not remove the document from the workflow only because it has no KSeF number before assessing the VAT deduction conditions.

This approach is more practical than the simple claim that every invoice outside KSeF is invalid. In reality, you need to determine whether you are dealing with an exemption, a special mode or a breach.

How to Prepare Before 2027

The year 2026 should be used to organise the invoicing process, not to build a habit of bypassing KSeF. The greatest risk appears when sales and accounting teams become comfortable working outside the system and then try to change everything only after penalties begin.

A good procedure starts with data. The invoice must be created as correct FA(3) XML, with consistent amounts, buyer data, dates and line items. A PDF can be a visualisation, but it is not the document submitted to KSeF.

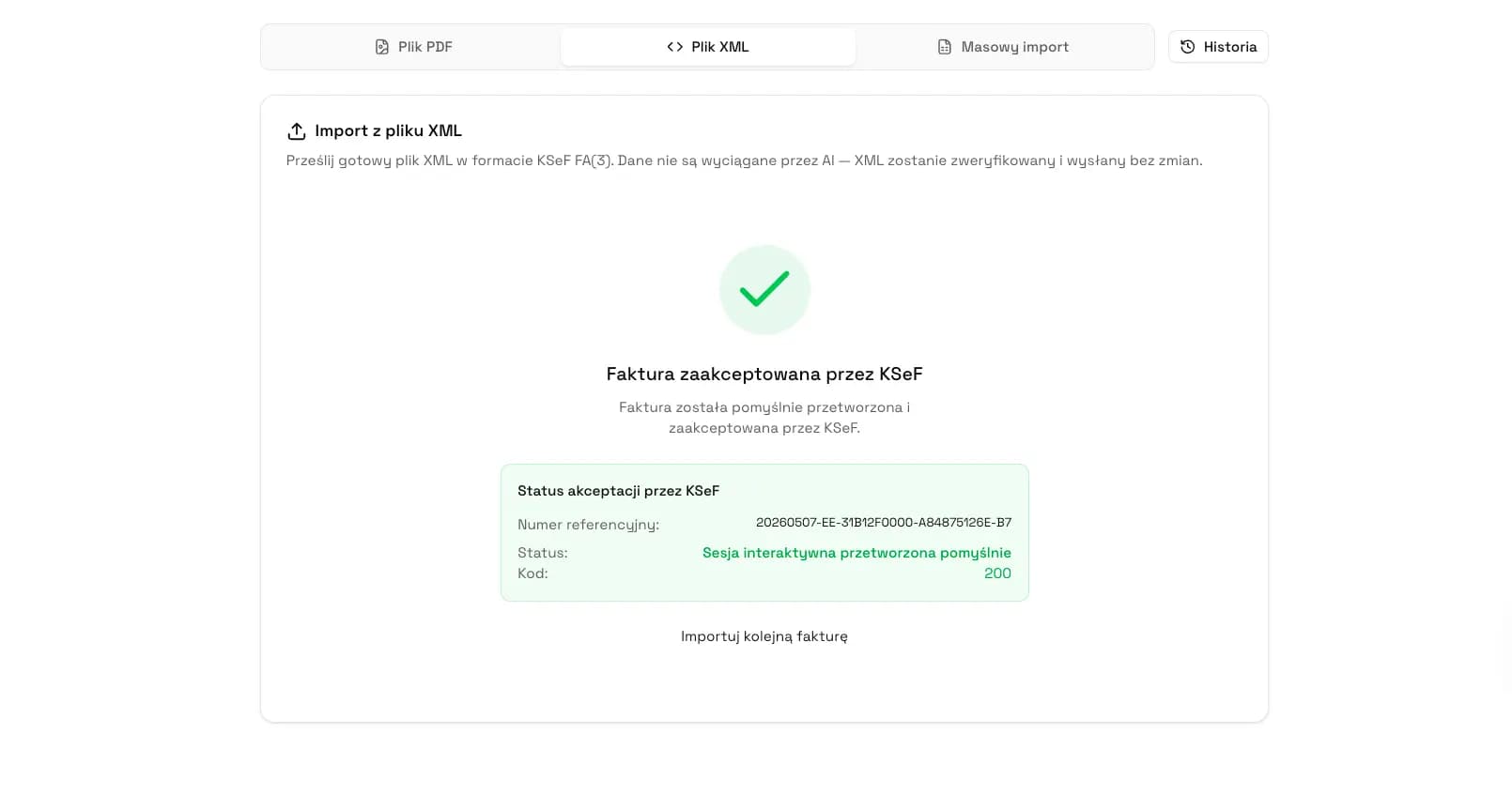

KSeFGPT can support KSeF document work: XML validation, preparation of structured invoices and organisation of submission statuses. To check a file before further processing, use the KSeF XML validator. You only need an email address, without creating a full account or paying. The free-plan limit is 5 validations per day.

Check XML before sending it to KSeF

Verify the invoice structure and catch technical errors before the document moves further in the process.

Open XML validatorCommon Wrong Assumptions

Mistake 1: Since there are no penalties in 2026, KSeF is voluntary. This is not true. The obligation may exist even when monetary sanctions are deferred.

Mistake 2: An invoice outside KSeF always removes the buyer's VAT deduction. This is too strong a simplification. MF points to the general deduction conditions and negative premises.

Mistake 3: Offline mode means a regular PDF invoice. No. A special mode requires following the rules and later submitting the invoice to KSeF.

Mistake 4: There will certainly be no penalties in 2027 either. Official sources do not support this claim. Currently, MF indicates penalties from 1 January 2027.

Official Sources

Scope of mandatory KSeF, podatki.gov.pl - implementation dates, temporary rules and exemptions.

KSeF rules and legal provisions, podatki.gov.pl - information on penalties from 1 January 2027.

KSeF FAQ, podatki.gov.pl - Ministry answers on invoices outside KSeF and VAT deduction.

Special invoice issuing modes, podatki.gov.pl - offline24, outage and KSeF unavailability rules.

Frequently Asked Questions

Can Polish businesses keep issuing invoices outside KSeF in 2026?

Only if the document or taxpayer falls under a clear exemption, or if a lawful special mode applies, such as offline24, outage or unavailability of KSeF. The temporary lack of financial penalties in 2026 does not remove the KSeF obligation.

Are there penalties for invoices issued outside KSeF in 2026?

Official Ministry of Finance materials indicate that monetary penalties for KSeF-related errors are not applied in the initial period of mandatory KSeF. This does not mean that every invoice outside KSeF is correct.

Will KSeF penalties apply from 2027?

According to official Ministry of Finance materials, KSeF penalties are expected to apply from 1 January 2027. They may concern, among other things, not issuing a structured invoice through KSeF despite the obligation, using the wrong structure in special modes, or failing to submit an offline invoice on time.

Does an invoice outside KSeF automatically block VAT deduction?

No. The Ministry of Finance indicates that VAT deduction may generally be available if the substantive conditions under Article 86 of the Polish VAT Act are met and no negative premises apply. Still, such an invoice should trigger a due-diligence check.

Should the buyer ask the seller to issue the invoice in KSeF?

The Ministry of Finance does not indicate a general obligation to request this after receiving an invoice outside KSeF. In practice, it is worth clarifying the situation when the seller should already be issuing structured invoices.

How can you distinguish an exemption from a KSeF breach?

Check the seller's mandatory KSeF date, the type of document, the buyer's status, the PLN 10,000 gross monthly threshold for 2026, and whether an offline or outage mode was used. If none of these fits, the case looks like a breach.

What should sellers do before 2027?

They should implement FA(3) XML generation, pre-submission validation, an offline24 procedure, archiving of KSeF numbers and UPO confirmations, and a clear distinction between B2B, B2C and excluded documents.

Recommendation

Do not build the process on the assumption that the lack of penalties in 2026 solves the problem. The safer practice is simple: classify every invoice outside KSeF as an exemption, a special mode or a case for clarification.

For the issuer, the priority is technical and procedural readiness before 2027. For the buyer, the priority is keeping transaction evidence and applying reasonable control to invoices that should appear in KSeF.

Prepare invoices for mandatory KSeF

KSeFGPT helps validate FA(3) XML files, organise invoice submission and monitor KSeF statuses.

Open KSeFGPTExpert reviewed: Marcin Kowalski

e-invoicing and KSeF integration expert · May 27, 2026

Review of official Ministry of Finance sources on invoices outside KSeF, VAT deduction and sanctions from 2027.

Related articles

New Invoice Notifications in KSeF

KSeF does not send an alert about a new invoice. See how KSeFGPT detects a new document and helps route it to the right person.

What is ViDA and how does it affect Polish businesses?

Understand ViDA's three pillars, the timeline through 2035 and what a Polish business can do now without implementing unsettled rules.

How to register for KSeF? Access, sign-in, permissions

There is no password-based KSeF account. Learn how authentication works, who gets automatic permissions, and when you need the ZAW-FA form.

How to create an invoice draft in KSeFGPT before sending it to KSeF

Save an invoice in progress as a draft or create one automatically from a PDF file. The document stays in KSeFGPT and is not sent to KSeF until you review and submit it yourself.