How to issue an invoice to a US company in KSeF

Check what data to collect from a US counterparty, how to approach VAT, FA(3) XML, the KSeF number and a readable English version.

Article Summary

An invoice for a US company in KSeF starts with the Polish issuer, not only with the buyer's country. If the seller is covered by the KSeF obligation, they need to check whether the document should be created as a structured invoice even when the counterparty does not have a Polish NIP.

The main practical risk is mixing three layers: the tax data of the transaction, the technical FA(3) XML and the readable version for the US counterparty. KSeF needs the correct structure, accounting needs the correct VAT treatment, and the counterparty usually needs an understandable PDF in English.

KSeFGPT can help with the operational process: collect counterparty data, issue the invoice, check XML, send the document to KSeF, save the status, KSeF number and UPO, and prepare a readable language version. It does not replace the tax decision on VAT rate, place of supply or supporting documents for the transaction.

Invoice a US customer in 2 minutes

Add a company without a Polish NIP, prepare the invoice in a form or in the AI Assistant Chat, send it to KSeF and download an English visualization without manual translation.

Issue an invoice in KSeFGPTWhere to start before issuing the invoice

Start by organizing responsibilities. KSeF answers how to issue and identify a structured invoice. Accounting answers how to settle a sale to a US company. The counterparty answers how they want to receive a readable version of the document outside the Polish system.

Collect these details before issuing: full legal name of the US company, address, country, tax identifier if it appears on the invoice, invoice email, currency, description of the supply, VAT decision, payment terms and the method of sharing the invoice after it is accepted in KSeF.

Do not assume that the US automatically excludes KSeF, that every document to the US has the same VAT rate, that an English PDF replaces XML, or that a foreign recipient will download the invoice themselves like a Polish taxpayer with a NIP.

Table of Contents

Key Takeaways

The table below gathers the decisions that need to be made before sending an invoice to KSeF and before sharing a readable version with the counterparty in the US.

| Point | Details |

|---|---|

| KSeF obligation | Assess mainly the situation of the Polish issuer and current exclusions, not only the buyer's country. |

| Buyer data | For a US company, do not force a Polish NIP. Determine the foreign identifier or use the correct no-identifier variant. |

| VAT and currency | XML validation does not decide tax treatment. Confirm the rate, currency and notes before submission. |

| Sharing the invoice | A US counterparty usually receives the invoice outside KSeF through an agreed method, with a visualization consistent with XML and the correct QR code. |

| KSeFGPT | The application helps with data, validation, submission, statuses, KSeF number, UPO and language version, but it does not replace accounting. |

How to issue an invoice to a US company in KSeF

The safest way to treat this topic is as a five-step process: first confirm the KSeF obligation on the Polish issuer side, then determine the US buyer data, then decide with accounting on VAT and currency, prepare a correct structured invoice, and finally share a readable version of the document with the counterparty.

Do not start with the question of whether the US customer has a KSeF account. For a Polish seller, it is more important to know whether the invoice has to be issued as a structured invoice and how to describe a buyer that does not have a Polish NIP. Only later do you decide on communication with the counterparty and sending a PDF or visualization.

Check in this order: the Polish issuer's KSeF status, buyer data, VAT decision, currency, XML correctness, sharing method outside KSeF and the complete submission trace, meaning KSeF number, status and UPO.

If you need broader context on the submission itself, read Sending invoices to KSeF. For the language version for the recipient, see KSeF invoice in English, German and Ukrainian.

| Step | What to check | Why it matters |

|---|---|---|

| KSeF obligation | Whether the Polish issuer is covered by KSeF and whether any specific exclusion applies. | A foreign buyer alone does not answer the question about the issuer's obligation. |

| Buyer data | Legal name, address, country and tax identifier if one appears. | Errors in counterparty identification may stop validation or make settlement harder. |

| VAT and currency | Type of sale, place of supply, currency, exchange rate and invoice description. | Sales to the US can have different tax effects depending on the transaction. |

| FA(3) XML | Whether the structure passes validation and contains consistent party and line-item data. | KSeF accepts a structured invoice, not an ordinary PDF. |

| Sharing | How the counterparty will receive a readable version outside KSeF. | A US company usually needs an operationally understandable version, often in English. |

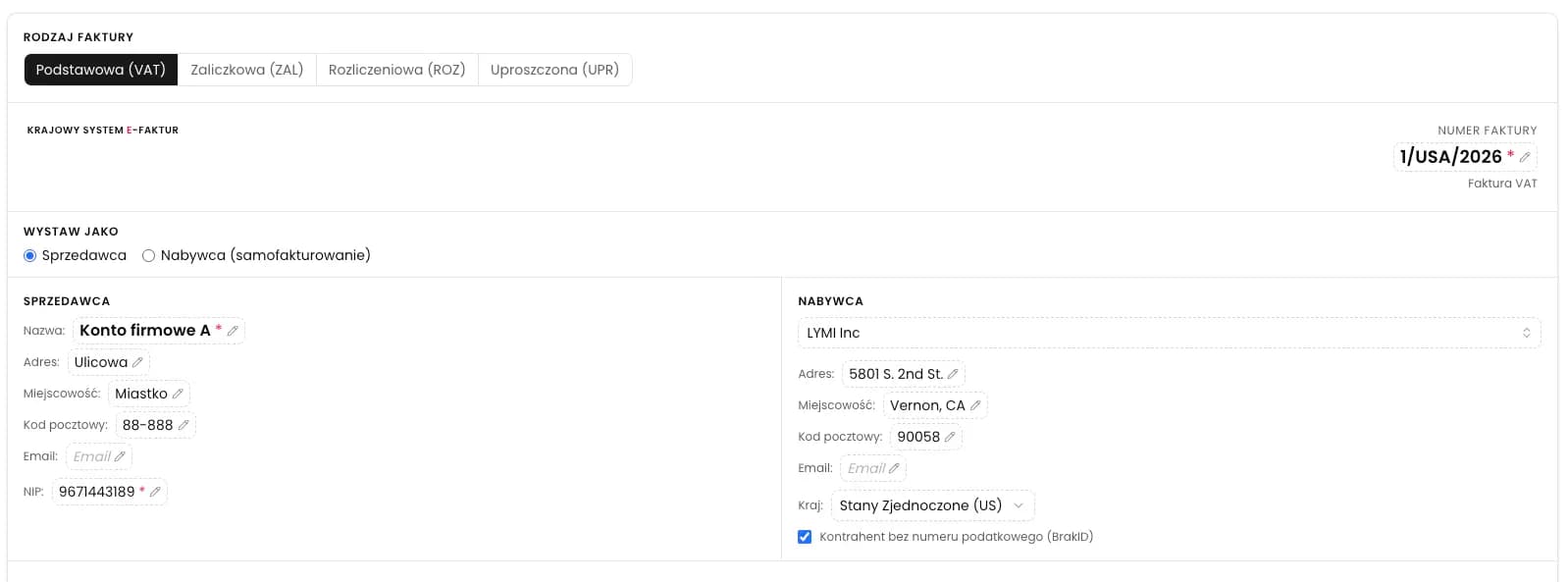

US counterparty data without a Polish NIP

In an invoice for a US company, do not try to force the buyer into a Polish NIP format. Start with the data that actually identifies the counterparty: full legal name, address, country, invoice email, contact person and tax identifier if the counterparty provides one and it should appear on the invoice.

The FA(3) schema supports different buyer identification variants. For a Polish buyer, the natural choice is NIP. For an EU counterparty, an EU VAT identifier may appear. For a non-EU entity such as a US company, another tax identifier with a country code may matter, or the no-identifier variant if no identifier appears on the invoice.

Data checklist: legal name, address, country US, tax identifier if it should appear on the invoice, invoice email address, contact person, purchase order or contract number, and visualization language for the recipient.

This does not mean that you should enter any number received in an email from the counterparty. Identification data should come from the contract, order, accounting data or confirmation from the counterparty. If the sales team only has a trade name, it is worth collecting full billing data before issuing the invoice.

| Data | Example check | Typical mistake |

|---|---|---|

| Legal name | Whether the name matches the contract or order. | Using a product name, branch name or abbreviation instead of the company name. |

| Address | Whether the address includes the country and full data needed for the invoice. | Entering only the city or a correspondence address without verification. |

| Country | Whether the buyer country is consistent with the address and identifier. | Leaving Poland as the default for a foreign counterparty. |

| Identifier | Whether the counterparty provided a tax identifier that should appear on the invoice. | Entering a Polish NIP in a field that does not apply to a US company. |

| Invoice email | Whether the address is used for document communication. | Sending the PDF to a sales contact instead of the finance department. |

VAT, currency and transaction description for the US

The most sensitive part of an invoice to the US is not technical, but tax-related. A service supplied to a company, a supply of goods, a license, subscription, consulting, export of goods or a service performed partly in Poland can each be assessed differently. That is why this article should not give one universal VAT rate for all invoices to the US.

Before issuing the document, agree with accounting what exactly you are selling, who the buyer is, where the place of supply or delivery is, what invoice currency applies, which exchange rate to use, whether a tax note is needed on the invoice and which documents support the transaction. Only after that decision does it make sense to move to the invoice form and XML.

Confirm with accounting: type of supply, place of taxation, currency, exchange rate, VAT rate or designation, line-item description, documents supporting the sale and the wording of any note for the counterparty.

In KSeF, the technical layer depends on FA(3) data consistency: dates, currency, items, amounts, rates, totals and party data must match. If the tax decision is uncertain, technical validation will not fix incorrect VAT treatment. It can say that the structure is correct, but not that the transaction has been assessed correctly for tax purposes.

| Question | Who should answer | Why before issuing |

|---|---|---|

| Is it goods, a service, a license or a subscription? | Sales and accounting. | The type of supply affects tax treatment. |

| Where is the place of supply or delivery? | Accounting or a tax adviser. | This determines how VAT and notes should be shown. |

| Which currency should the invoice use? | Contract and accounting. | The currency must match the contract, payment and conversions. |

| Is an additional note needed? | Accounting. | The counterparty and audit trail should make the settlement method clear. |

| Which documents support the transaction? | Sales, accounting and logistics. | The invoice alone is not always enough to defend the settlement. |

Does a US company receive the invoice through KSeF?

A domestic buyer with a Polish NIP can receive invoices in KSeF in the standard flow. With a US counterparty, the practical situation is different: the buyer may not use KSeF, may not have a Polish identifier and may expect normal email communication or a procurement portal. That is why, apart from issuing the invoice itself, you need to plan how to share a readable version of the document.

In practice, for buyers without a registered office or fixed establishment in Poland, the invoice is shared outside KSeF in a way agreed with the buyer. This may be an email with a PDF, the counterparty's portal or another agreed channel, but the form should allow the recipient to read the document and verify it according to KSeF rules.

Do not confuse sharing outside KSeF with claiming that the PDF is the source invoice. The source layer for KSeF is FA(3) XML, and after acceptance also the KSeF number and UPO. An English PDF is a practical human-readable visualization that helps the counterparty book the document, approve payment and pass it internally.

For an invoice shared outside KSeF, remember the verification QR code and the access or identification data required to verify the document. For an invoice issued online after acceptance by KSeF, the KSeF number is crucial. Offline modes may introduce additional markings, so do not treat any PDF without the proper elements as a complete sharing process.

Agree with the counterparty: sending channel, visualization language, email address or portal, information about the KSeF number, document verification method and the person on the customer side responsible for payment.

In an email to a US company, describe the attachment neutrally: as an informational visualization of an invoice issued in the Polish KSeF system. Avoid wording that suggests a second invoice has been created or that the English PDF replaces the source data. The difference between PDF, XML, KSeF number and UPO is explained more broadly in Translated KSeF invoice, PDF, XML and UPO.

| Layer | Role | What to share with the counterparty |

|---|---|---|

| FA(3) XML | Invoice data in the KSeF structure. | Usually keep it in the archive and accounting system, unless the counterparty requires the file. |

| KSeF number | Invoice identifier after acceptance by KSeF. | It can be included in the description or on the visualization if it helps identification. |

| UPO | Operational confirmation that the document was accepted. | Usually for the issuer, accounting and audit, not as the main customer document. |

| English PDF | Readable visualization for the recipient. | Most often the best attachment for the finance department in the US. |

How KSeFGPT helps with an invoice for a US company

KSeFGPT should not be described as a tax adviser or a government system. Its role is operational: it helps prepare and control invoice data, work with counterparties, validate XML, send the document to KSeF and organize statuses after submission.

With a US company, three elements are especially useful. First, the counterparty database helps avoid retyping the name, address and contact data every time. Second, the Invoices module supports outgoing FA(3) invoices, validation and submission. Third, PDF language versions help share a readable document with a person who does not work in Polish.

Operational example: a Polish SaaS company issues a monthly invoice to a Delaware company. In KSeFGPT, it saves the counterparty data, confirms VAT treatment with accounting, checks XML, sends the invoice to KSeF and, after acceptance, downloads an English visualization for the customer's finance team.

The supported visualization language versions in KSeFGPT are Polish, English, Ukrainian and German. For a US counterparty, you will usually choose English, but the same process also helps when the document must go to a team working in German or Ukrainian.

A good KSeFGPT process looks like this: prepare the counterparty, issue the invoice, check the data and XML, send the document to KSeF, save the status, KSeF number and UPO, and then share a readable visualization with the counterparty. If the VAT treatment is uncertain, stop the process before submission and confirm it with accounting.

| Stage in KSeFGPT | What it helps do | What it still does not replace |

|---|---|---|

| Counterparty | Organize the name, address, country, email and contact data. | Tax verification of the counterparty and contract. |

| Invoice | Prepare document data and go through the preview before submission. | Decision on place of supply and VAT rate. |

| XML validation | Detect problems in the FA(3) structure, dates, amounts and required fields. | Assessment of whether the US sale is classified correctly. |

| Submission and status | Keep the status, KSeF number and UPO after the document is accepted. | A guarantee of payment by the counterparty. |

| Language version | Download a visualization in Polish, English, Ukrainian or German. | The source XML or an official certified translation. |

Issue and control KSeF invoices in one process

KSeFGPT helps organize counterparty data, check the invoice, send XML to KSeF and share a readable document version with the recipient.

Go to KSeFGPTCommon mistakes when invoicing a US company

The first mistake is assuming that because the buyer is from the US, KSeF disappears from the process. This simplification can be risky, because the obligation to issue a structured invoice is assessed mainly from the perspective of the Polish issuer and the scope of the regulations, not only by the buyer's country.

The second mistake is treating XML validation as confirmation of the correct VAT rate. A technically correct file may still contain incorrect transaction classification. That is why the VAT decision, currency, description and supporting documents should be prepared before clicking send.

The third mistake is sending the counterparty a Polish visualization without explaining what KSeF is and what the KSeF number means. A US company may need a simple email in English, a readable PDF and clear information that the source invoice was issued in the Polish e-invoicing system.

| Mistake | Consequence | Safer practice |

|---|---|---|

| Skipping KSeF because of the buyer's country | Risk of issuing the document outside the required process. | First check the obligation on the Polish issuer side. |

| Entering a random identifier | Chaos in buyer data and possible validation problems. | Collect billing data from the contract or counterparty confirmation. |

| One VAT rate for all invoices to the US | Incorrect transaction settlement. | Confirm classification with accounting for the specific sale. |

| PDF as the only process trace | No full proof of acceptance and identification in KSeF. | Keep XML, KSeF number, status and UPO. |

| No readable version for the recipient | Questions and delays on the counterparty side. | Send a readable English visualization with a neutral explanation. |

Expert perspective: KSeF does not solve tax for you

KSeF changes the form and technical trace of an invoice, but it does not remove the classic tax questions involved in international sales. You still need to know what is being sold, where the place of supply is, who the buyer is and which documents support the transaction.

In practice, the best process is not a salesperson entering a few data points into a system and expecting the validator to decide everything automatically. The validator should check the structure and data consistency. The tax decision should be prepared earlier and, in non-standard cases, confirmed by accounting or an adviser.

A good KSeF application helps reduce operational errors: it does not lose the KSeF number, shows the status, allows UPO download, stores counterparty data and supports communication. It should not promise that choosing a form will replace analysis of a US transaction.

Frequently Asked Questions

Does an invoice for a US company have to be issued in KSeF?

If the Polish issuer is covered by the KSeF obligation and no specific exclusion applies, an invoice for a US company may still have to be prepared as a structured invoice. The fact that the buyer is foreign and does not have a Polish NIP should not be treated automatically as an exemption from KSeF control.

What should be entered instead of a NIP for a US counterparty?

For buyer data, collect the legal name, address, country and tax identifier used by the counterparty if it appears on the invoice. The FA(3) schema allows different buyer identification variants, including another tax identifier with a country code or BrakID when no identifier appears on the invoice.

Does a US company receive the invoice directly in KSeF?

Usually you should not assume that a US counterparty will receive the invoice in the same way as a domestic buyer with a Polish NIP. In practice, you need to agree on a sharing method outside KSeF, for example a readable PDF or visualization with the correct QR code and data that allow the document to be verified, while keeping the FA(3) XML, KSeF number and UPO on the issuer side.

Does KSeFGPT decide VAT treatment for sales to the US?

No invoicing tool should be treated as a substitute for a tax decision. KSeFGPT helps organize invoice data, prepare XML, validate the document, send it to KSeF and keep statuses, but VAT treatment depends on the type of transaction and should be confirmed with accounting.

Recommendation

If you are issuing your first invoice to a US company, start with a correct KSeF process and clear communication with the counterparty, and only then optimize automation.

For the recipient language version, read KSeF invoice in English, German and Ukrainian. If you want to distinguish PDF, XML and UPO, return to Translated KSeF invoice, PDF, XML and UPO.

For submission and statuses, the guide Sending invoices to KSeF will be useful. If you want to control identifiers after submission, also read KSeF number on invoice.

Issue invoices for foreign counterparties without chaos

KSeFGPT helps prepare invoice data, check FA(3) XML, send the document to KSeF and share a readable document version with the counterparty.

Go to KSeFGPTSources and Reference Materials

The article is based on official KSeF 2.0 materials, the FA(3) schema, the VAT Act and the locally verified scope of KSeFGPT features. Sources were checked on July 7, 2026.

- Scope of Mandatory KSeF

KSeF · accessed: July 7, 2026

Official information on the stages of mandatory KSeF, the scope of invoice issuing and exclusions from the obligation.

- Structured Invoice and FA Logical Structure

KSeF · accessed: July 7, 2026

Official description of a structured invoice, the FA structure and the basic distinction between an invoice in KSeF and a visualization.

- Issuing and Receiving Invoices in KSeF

KSeF · accessed: July 7, 2026

Ministry of Finance material on issuing, receiving and sharing invoices, including the receipt date and exceptions for buyers outside the standard KSeF flow.

- KSeF 2.0 Handbook, Part II - Issuing and Receiving Invoices in KSeF

Ministry of Finance · accessed: July 7, 2026

Ministry of Finance handbook describing practical rules for issuing and receiving invoices and sharing invoices outside KSeF in specified cases.

- FA(3) Schema v1-0E

CIRF / Ministry of Finance · accessed: July 7, 2026

Official FA(3) XSD schema, including buyer identification, address, currency, line items and invoice type elements.

- KSeF Number and Collective Identifier

KSeF · accessed: July 7, 2026

Official explanation of the KSeF number, its role after invoice acceptance and the difference from the invoice's own number.

- QR Verification Codes

KSeF · accessed: July 7, 2026

Official rules for marking invoices shared outside KSeF with a QR verification code and the distinction between online and offline invoices.

Expert reviewed: Bogdan Mazurek

Tax adviser · July 7, 2026

Reviewed the distinction between the KSeF obligation on the Polish issuer side, the technical FA(3) structure, sharing an invoice with a foreign counterparty and the need for separate VAT classification for US transactions.

Related articles

MPP on KSeF invoices after an individual interpretation

Analysis of the dispute over voluntary split payment in KSeF: where the technical invoice marking ends and the tax risk of overinterpretation begins.

How to Issue a Final Invoice After an Advance in KSeF

Learn when a final invoice is needed after an advance, how to deduct earlier payments and avoid settling the same sale twice.

From LiveKid to KSeF: PDF invoices and settlements

LiveKid provides a PDF invoice, PDF correction and settlement, but does not send them to KSeF. See how to turn a PDF into FA(3) XML and submit the invoice to KSeF.

How to check invoice status in KSeF after submission?

You sent an invoice to KSeF, but you do not know whether it has been accepted, is still being processed, or was rejected? Check the status, reference number, KSeF number and UPO step by step.